The stock markets are mixed after the hawkish rate cut by Fed overnight but treasury yields are back under pressure. Dollar rose mildly after the announcement but there was no follow through buying. Yen surges broadly today, riding on falling yields, followed by Swiss Franc. Australian Dollar is the weakest one on rise in unemployment rate, followed by New Zealand Dollar.

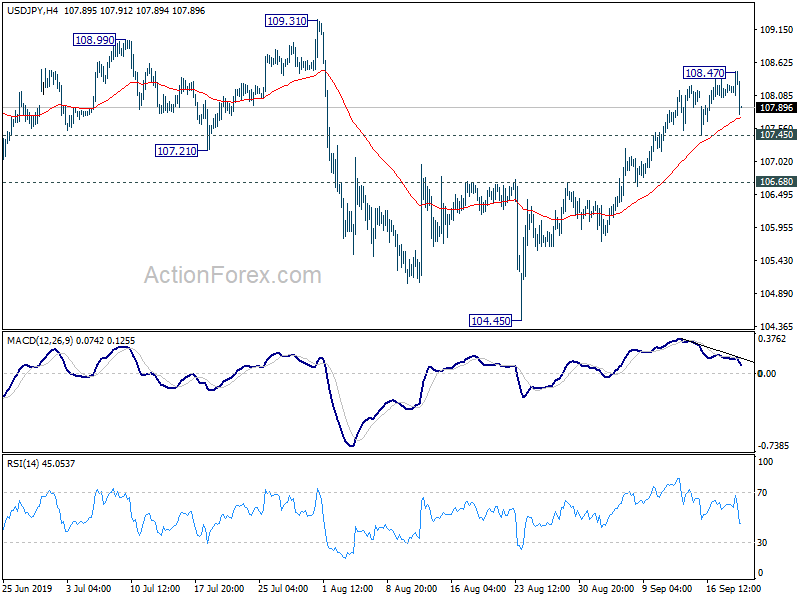

Technically, AUD/USD’s break of 0.6807 minor support suggests completion of corrective rebound from 0.6677. Further fall should be seen to retest this low. EUR/AUD’s rebound from 1.5905 is accelerating and break of 1.6308 could pave the way back to 1.6786 high. USD/JPY lost momentum well ahead of 109.31 resistance. Focus is back on 107.45 minor support and break will bring deeper fall back towards 104.45 low.

In Asia, Nikkei is up 0.52%. Hong Kong HSI is down -1.24%. China Shanghai SSE is flat. Singapore Strait Times is down -0.20%. Japan 10-year yield is down -0.0348 at -0.217. Overnight, DOW rose 0.13%. S&P 500 rose 0.03%. NASDAQ dropped -0.11%. 10-year yield dropped -0.026 to 1.786.

FOMC Cut Rate by -25 bps, mid-cycle adjustment could be done

Fed cut the policy rate by -25 bps to 1.75-2.00% as expected. The decision was not unanimous as three voters dissented. Boston Fed President Rosengren and Kansas City Fed President Esther George voted to maintain the policy rate unchanged. This has been expected as they did the same previously. The surprise came from St. Louis Fed President James Bullard who proposed a deeper cut of -50 bps.

The economic projections were little changed from June, although the members expressed greater concerns about the trade war uncertainty. The median projections of federal funds rate are at 1.9% in 2019 and 2020, then rises to 2.1% in 2021. Just based on this median figure, with federal funds rate at 1.75-2.00%, Fed is already done with it’s “mid-cycle” adjustments.

However, based on the dot plot, it’s not totally certain and there is still risk of further rate cut this year. 7 members have penciled in another cut to 1.50-1.75% this year. 10 members have penciled in rate between 1.75 and 2.25%. Some of the “hawks” could switch if outlook worsens.

Suggested readings:

- FOMC Cut Rate by -25 bps. Third Cut Still Possible Despite Sounding Less Dovish

- Fed Cuts Rates 25 Bps. Is Further Easing On The Way?

- FOMC Review: Fed Cut With No Quick Fix To Tight Liquidity Conditions

- Northern Exposure: FOMC to Continue to “Act as Appropriate”

- FOMC Recap: Hawkish Cut Confirmed as Most Fed Members Don’t Expect Another Cut This Year!”

- Divided Fed Cuts Rates Again

- Dollar higher after Fed’s hawkish cut, upside limited so far

- Fed downgrades median rate projections to 1.9% in 2019, dot plot shows no more cut

- Fed cut by -25bps with 7-3 vote, Bullard wants -50bps cut

BoJ stands pat, global downside risks increasing

BoJ left monetary policy unchanged as widely expected. Under the yield curve control framework, short-term policy rate is kept at -0.1%. The central bank will continue JGB purchases to keep 10-year yield at around 0%. Annual monetary base expansion will be kept at around JPY 80T.

On the outlook, BoJ expects that the economy is “likely to continue on a moderate expanding trend, despite being affected by the slowdown in overseas economies”. Domestic demand is “expected to follow an uptrend”. Exports are “projected to show some weakness”, but still be on a “moderate increasing trend”. CPI is likely to increase “gradually toward 2 percent”.

Risks include US macroeconomic policies, protectionism, emerging markets, global adjustments in IT goods, Brexit and geopolitical risks. BoJ warned that “downside risks concerning overseas economies seem to be increasing, and it also is necessary to pay close attention to their impact on firms’ and households’ sentiment in Japan.”

Australia employment grew 34.7k, unemployment rate rose to 5.3%

Australian employment grew 34.7k in August, well above expectation of 20k. Full-time employment rose 7.2k while part-time employment added 14.7k. Unemployment rate rose 0.1% to 5.3%, above expectation of 5.2%. At the same time, participation rate rose 0.1% to 66.2%.

In seasonally adjusted terms, from July 2019 to August 2019, the largest increases in employment were in Victoria (up 20,300 persons) and New South Wales (up 16,700 persons). The largest decrease was in Queensland (down 7,200 persons). The seasonally adjusted unemployment rate increased by 0.4 pts in South Australia (7.3%) and Tasmania (6.4%), and by 0.1 pts in Victoria (4.9%). Decreases were recorded in New South Wales (down 0.2 pts to 4.3%) and Western Australia (down 0.1 pts to 5.8%), with Queensland recording no change.

New Zealand GDP grew 0.5%, services led

New Zealand GDP grew 0.5% qoq in Q2, above expectation of 0.4% qoq. Services industries grew 0.7%, accelerated from 0.3%. Services growth was also wide-spread, in 8 out of 11 industries. Primary industries expanded 0.7%, rebound from two consecutive declines. However, goods-producing industries fell -0.2%, following 1.9% rise back in Q1.

Looking ahead

Both SNB and BoE are expected to keep monetary policies unchanged today, and no surprise is expected there. Swiss will release trade balance while UK will release retail sales. Eurozone will release current account. Later in the day, US will release Philly Fed survey, jobless claims, leading indicator, exiting home sales and current account balance.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.20; (P) 108.34; (R1) 108.59;

USD/JPY retreats sharply after hitting 108.47. Intraday bias is turned neutral again. Further rise cannot be ruled out as long as 107.45 support holds. But we’d continue to look for topping sign as it approaches this 109.31 key resistance. On the downside, break of 107.45 minor support will suggest that rebound from 104.45 has completed. Intraday bias will be turned back to the downside. Break of 106.68 resistance turned support will confirm and target 104.45 low. However, decisive break of 109.31 will carry larger bullish implication.

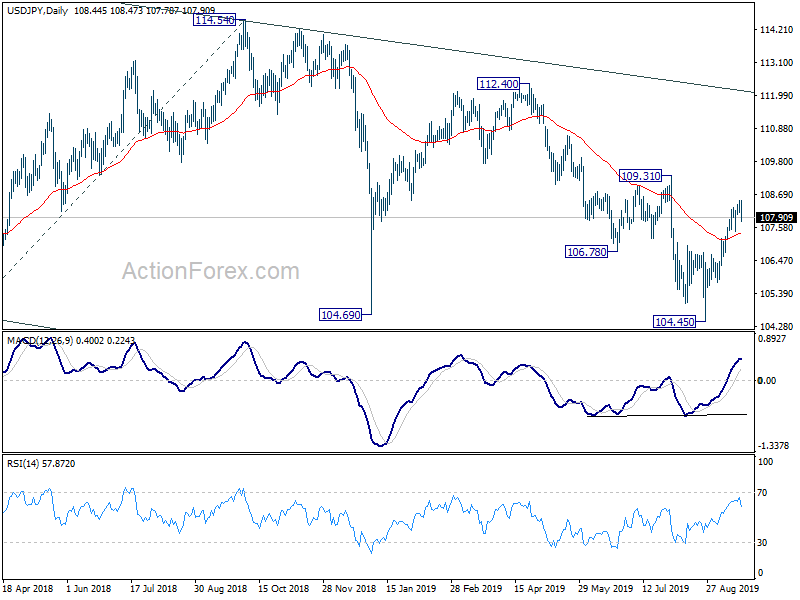

In the bigger picture, decline from 118.65 (Dec 2016) is still in progress and the pair is staying well inside long term falling channel. Firm break of 104.69 will target 100% projection of 118.65 to 104.62 from 114.54 at 100.51. For now, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. However, firm break of 109.31 will be the first sign of medium term reversal and bring stronger rise to 112.40 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | 0.50% | 0.40% | 0.60% | |

| 1:30 | AUD | Employment Change Aug | 34.7K | 20K | 41.1K | |

| 1:30 | AUD | Unemployment Rate Aug | 5.30% | 5.20% | 5.20% | |

| 4:30 | JPY | All Industry Activity Index M/M Jul | 0.40% | -0.80% | ||

| 6:00 | CHF | Trade Balance (CHF) Aug | 3.22B | 3.63B | ||

| 7:30 | CHF | SNB Policy Rate | -0.75% | -0.75% | ||

| 8:30 | GBP | Retail Sales Inc Auto Fuel M/M Aug | 0.00% | 0.20% | ||

| 8:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Aug | 2.90% | 3.30% | ||

| 8:00 | EUR | Eurozone Current Account (EUR) Jul | 20.3B | 18.4B | ||

| 8:30 | GBP | Retail Sales Ex Auto Fuel M/M Aug | 0.00% | 0.20% | ||

| 8:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Aug | 2.60% | 2.90% | ||

| 11:00 | GBP | BoE Bank Rate | 0.75% | 0.75% | ||

| 11:00 | GBP | BoE Asset Purchase Target Sep | 435B | 435B | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–0–09 | 0–0–09 | ||

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–09 | 0–0–09 | ||

| 12:30 | CAD | ADP Payroll Estimates Aug | 73.7K | |||

| 12:30 | USD | Current Account Balance (USD) Q2 | -127B | -130B | ||

| 12:30 | USD | Philadelphia Fed Business Outlook Sep | 10.8 | 16.8 | ||

| 12:30 | USD | Initial Jobless Claims (SEP 14) | 210K | 204K | ||

| 14:00 | USD | Leading Index Aug | 0.10% | 0.50% | ||

| 14:00 | USD | Existing Home Sales Aug | 5.39M | 5.42M | ||

| 14:30 | USD | Natural Gas Storage | 78B |

Hot

No comment on record. Start new comment.