The war in Ukraine and inflation fears were the dominant themes this week, sparking a move towards commodities. This is likely why we saw the Comdolls out perform against the majors, including the safe havens, in this wartime environment.

Notable News & Economic Updates:

US, EU, UK, Japan agree to remove selected Russian banks from SWIFT

U.S. EIA crude oil inventories slid 2.8M barrels vs. projected 2.5M gain

Oil jumps to highest since 2011 as OPEC holds output steady despite Russia’s war on Ukraine

Commodities hit new highs as traders stay clear of Russian products

Fed Chair Powell says still open to 50 bps hike in March if high inflation persists

Swiss City of Lugano to make bitcoin and Tether ‘De Facto’ legal tender

Switzerland imposes sanctions on Russia; breaks its historically neutral geopolitical stance

S&P ratings agency cutting Russia’s credit ratings by eight levels to “CCC-minus”

More than 90% of U.S. population can ditch facemasks under CDC Covid guidance

Russian forces shell and take Zaporizhzhia nuclear power plant in Ukraine; sparking fears of a nuclear disaster on Friday.

Intermarket Weekly Recap

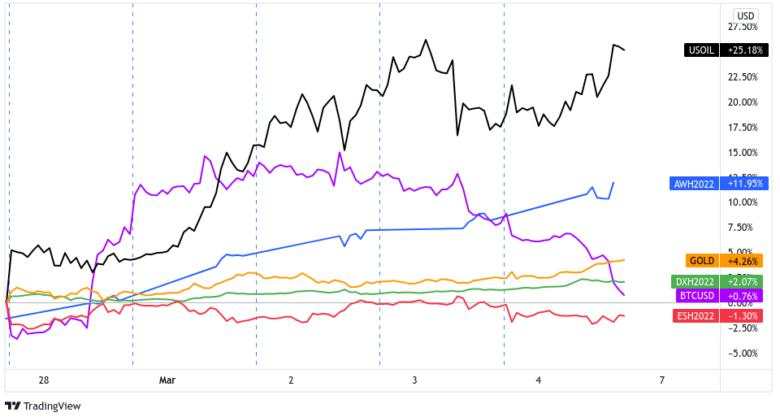

Dollar, Gold, S&P 500, Oil, Commodity Index, Bitcoin Overlay 1-Hour

Russia-Ukraine war developments continued to dominate headlines this week, with traders now having to focus on the sanctions placed on Russia and their potential impact on the global economy.

Countries around the world have taken actions to put pressure on the Russian government to stop the invasion, most notably the removal of several Russian banks from the SWIFT international payments messaging system, as well as freezing the assets of wealthy Russia citizens in foreign accounts.

There were also discussions of potentially placing sanctions on Russian exports, which is largely made up of energy and commodity products. This understandably added fuel to inflation fears as the potential reduction of commodities in the market (especially energy products) was likely the spark that pushed traders to buy up commodities this week.

The Bloomberg Commodity Index is up ~12% to 126.00 from the Friday close, oil is easily holding above $100 per barrel now, and gold (up over 4% this week) is not too far away from testing the $2,000 psychological handle.

Another notable story this week was the pop higher in bitcoin and other crypto assets on Monday, possibly a reaction to a slew of headlines including the collapse in the Russian Ruble (ruble fell 45% against USD to ~122), fears of a bank run in Russia, and how Ukraine is accepting support through crypto donations, raising over $35M in various crypto assets.

Outside of the dire situation between Russia and Ukraine, monetary policy headlines sparked some action this week, most notably from Federal Reserve Chair Powell during the semi-annual monetary policy report to Congress. Powell kept the door open for a 50 bps hike on Thursday, likely dampening recent speculation that geopolitical events could prompt the Fed to only hike by 25 bps in the upcoming March meeting.

In forex, the Aussie and Kiwi took the top spots, likely benefiting from the swift rise in commodity prices and a round of net positive economic updates from Australia (supporting rate hike expectations in the region).

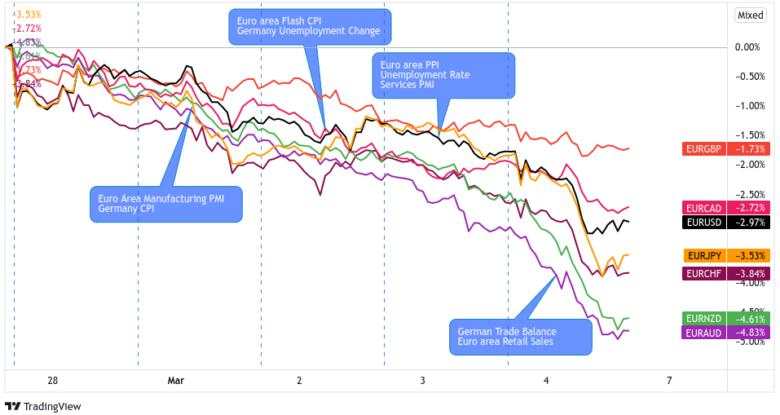

The euro is the biggest loser this week, not only likely driven by the violence right outside of the Euro area in Ukraine, but also likely on traders pushing back expectations that the European Central Bank will tighten interest rates in June to September.

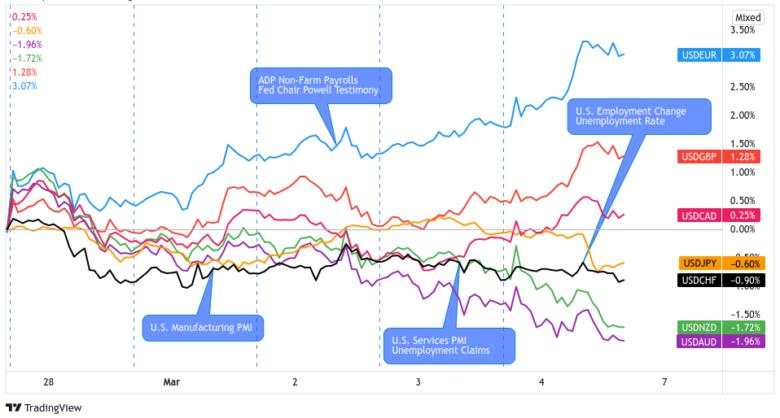

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

U.S. ISM manufacturing PMI rises to 58.6 in Feb vs. 58.0 expected

U.S. construction spending surges +1.3% in January on home building vs. +0.8% in December

Atlanta Fed Chief Bostic says 0.50% hike possible if inflation persists

Fed Chair Powell notes ‘highly uncertain’ Ukraine impact, but says rate hikes are still coming

ADP non-farm employment change posted 475K gain in Feb, previous reading upgraded

ISM Services PMI: 56.5 in February vs. 59.9 in January

U.S. unemployment rate falls to 3.8%; added 678K jobs; previous two months revised higher

Fed Evans says rates may rise to near 2% in 2022 after strong jobs report

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

UK mortgage approvals for house purchases rose to 74,000 in January

IHS Markit/CIPS U.K. manufacturing PMI: 58.0 in February vs. 57.3 in January; a three-month high

BoE’s Saunders sees inflation risks but might not back big hike again

UK Construction PMI in February: 59.1 vs. 56.3 in January

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

Spanish manufacturing PMI up from 56.2 to 56.9 vs. 55.9 forecast

Germany Manufacturing PMI: 58.4 in February vs. 59.8 in January

ECB Monetary Policy Meeting Accounts: 2-3 February 2022

- “Mr Lane stressed that the euro area economy continued to recover, although it was likely to remain subdued in the first quarter of 2022”

- There are signs that supply bottlenecks might be starting to ease

- Risks to the growth outlook remained broadly balanced over the medium term

- Geopolitical tensions have increased, potentially prolonging high energy costs. This is a material downside risk to investment and consumer spending, while also increasing cost pressures in energy-intensive sectors.

German exports (+7.5% y/y) rose at a slower pace than imports (+22.1% y/y) in Jan

France’s industrial production up by 1.6% vs. 0.6% expected in Jan

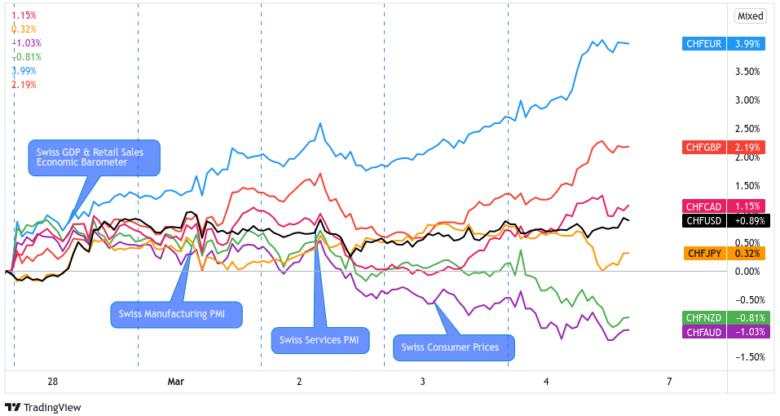

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

Swiss retail trade turnover increased by 4.8% in January 2022

KOF Swiss Economic Barometer dips to 105.04 in Feb. vs. 107.21 in January

Swiss service sector boosted in February by easing COVID-19 restrictions – Procure

Switzerland imposes sanctions on Russia; breaks its historically neutral geopolitical stance

Swiss CPI: +2.2% y/y vs. 1.8% y/y forecast

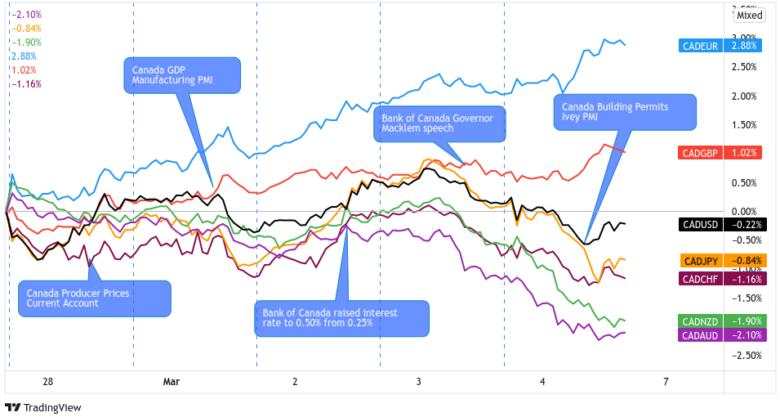

CAD Pairs

Overlay of CAD Pairs: 1-Hour Forex Chart

Canada’s current account balance: $0.8B deficit in the fourth quarter of 2021 vs. $0.8B in previous quarter.

Canada Industrial Product Price Index (IPPI): +3.0% m/m in January 2022

Canadian GDP: +1.6% q/q in the Q4 of 2021, following a 1.3% rise in Q3

Canada Manufacturing PMI: 56.6 in February vs. 56.2 in January – IHS Markit

Bank of Canada raised interest rates to 0.50% from 0.25% on Wednesday

Canadian building permits decreased 8.8% to $10.1B in January

Canada’s Ivey PMI rose to 60.6 in February from 50.7 in January; employment gauge rose to 60.3 from 49.1

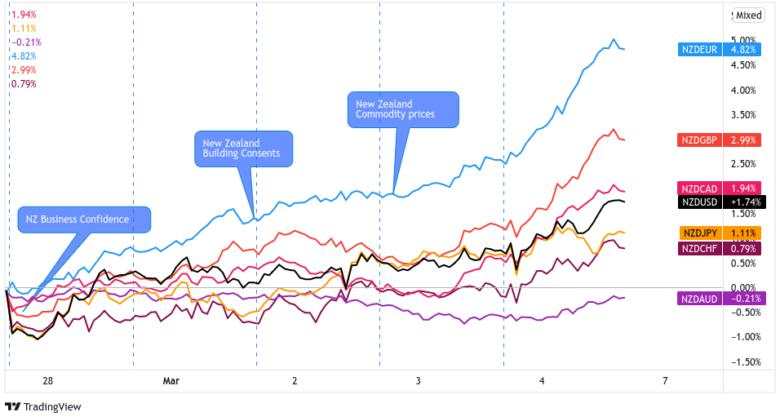

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

Global Dairy prices rise +5.1% since last auction

New Zealand commodity prices rose 3.9% according to ANZ

New Zealand Building Consents falls -9.2% in January

ANZ-Roy Morgan NZ Consumer Confidence: -16 to a record low of 81.7 in February

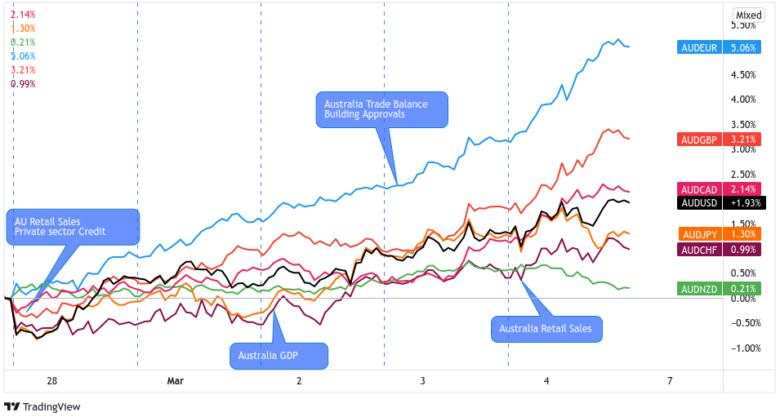

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

Australia’s company gross profits rise 2.0% In Q4

Australia retail sales rebound by 1.8% in January (after 4.4% drop in December) as economy weathers Omicron

Australian AIG manufacturing index up from 48.4 to 53.2

RBA kept interest rates on hold at 0.10% as expected; says Australian economy resilient, spending picking up after Omicron setback

Australia’s GDP rebounds by 3.4% in Q4 2021 vs. 3.5% expected, -1.9% in Q3

Australia’s AIG construction index rose from 45.9 to 53.4

Australian building approvals slumped 27.9% vs. projected 2.9% dip

Australia’s trade surplus widened from 8.82B AUD to 12.89B AUD

AU retail sales rebound from 4.4% drop in Dec to 1.8% gain (the second-highest increase on record) in Jan.

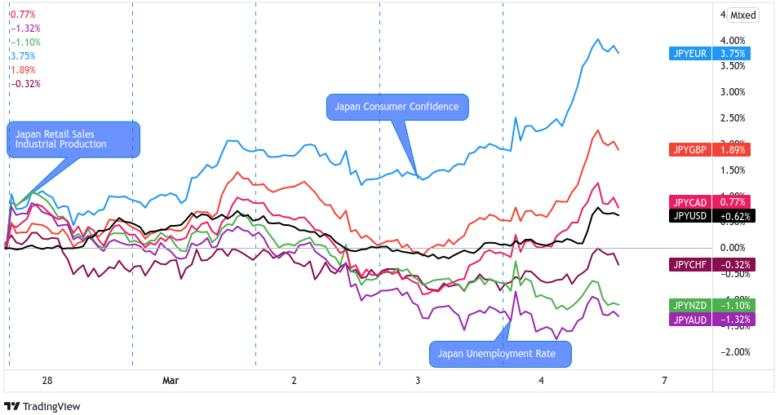

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Japan industrial production drops 1.3% on month in January

Japan retail sales rise 1.5% y/y in January

Japan housing starts growth eases from 4.2% to 2.1% in January

Japanese final manufacturing PMI downgraded from 52.9 to 52.7

The final au Jibun Bank Japan Services PMI fell to 44.2 in Feb. vs. 47.6 previous; fastest pace in 21 months

Ukraine crisis may hurt Japan’s economy via fuel spike, says BOJ policymaker

Fuel spike may push Japan’s inflation near BOJ’s 2% goal, says policymaker

Japan’s unemployment rate up from 2.7% to 2.8% in Jan as COVID wave prompted restrictions

Japan unveil plan to boost oil subsidy and back small firms to soften blow from rising energy prices

Hot

No comment on record. Start new comment.