Markets started the week with dramatic moves as China promised looser policies and Syria’s Assad regime collapsed over the weekend, shaking up commodities and equities.

Gold got a boost from safe-haven demand and Chinese stimulus hopes, while tech stocks took a hit on renewed regulatory worries—all amid a cautious mood ahead of key inflation data.

Here are the major market themes that started the week with a bang!

Headlines:

- Over the weekend, Syrian President Assad fled to Moscow as rebels took Damascus, ending over five decades of Assad rule

- Over the weekend, PBOC reported it had resumed gold-buying after a six-month break in November

- China’s 24-man Politburo, China’s top decision-making body, pledged to implement “more active fiscal policies and moderately loose monetary policies”

- China opened a probe into Nvidia Corp. over anti-monopoly laws potentially broken in a 2020 deal

- Japan final Q3 GDP revised higher from 0.9% y/y to 1.2% y/y; GDP price index eased from 2.5% y/y to 2.4% y/y (2.5% expected)

- China’s annual CPI slowed from 0.3% to a five-month low of 0.2% in November; Annual PPI slowed its deflation from -2.9% to -2.5%

- Japan Economy Watchers sentiment improved from 47.5 to 49.4 (47.3 expected) in November

- Switzerland SECO consumer climate index steadied at -37 (-38 expected) in November

- Eurozone Sentix investor confidence index worsened from -12.8 to -17.5 (-12.4 expected) in December, the lowest since November 2023

- New York Fed one-year inflation expectations rose from 2.9% to 3.0% in November; Three-year inflation estimates edged up from 2.5% to 2.6%

Broad Market Price Action:

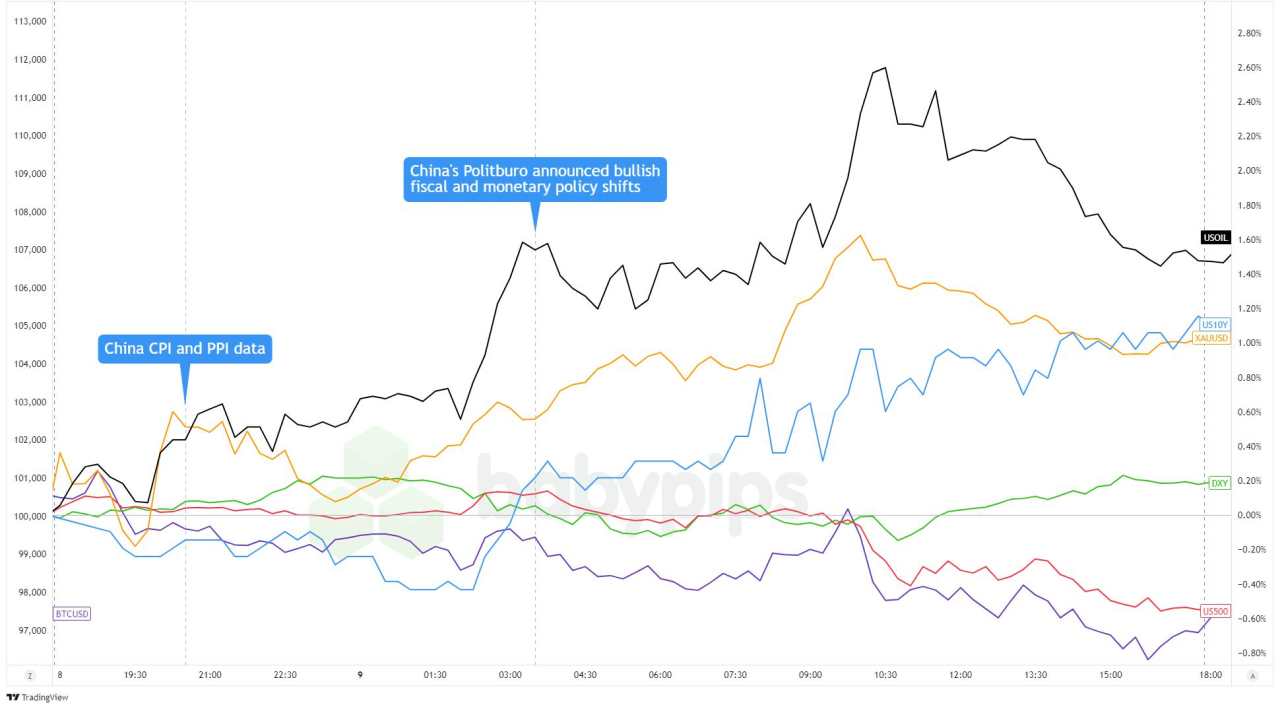

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Markets kicked off the week with sharp price swings, driven by weekend headlines and positioning ahead of potential catalysts scheduled later this week.

Gold and oil rallied following a dramatic regime change in Syria, with President Assad reportedly fleeing to Moscow after rebels seized Damascus. China’s Politburo pledging a “more proactive” fiscal policy and “moderately loose” monetary stance, alongside the PBOC resuming gold purchases after a six-month pause, further boosted commodity demand. Gold hit fresh two-week highs near $2,675, while U.S. crude oil climbed 1.7% to $68.80.

Equities painted a mixed picture—Asian markets struggled with weak Chinese inflation data and South Korean uncertainty, but European mining stocks got a lift from China’s stimulus hints. U.S. stocks didn’t fare as well, with the S&P 500 slipping as Nvidia faced an anti-monopoly probe from China, and traders potentially locked in profits ahead of this week’s CPI data. Bitcoin also eased lower, dropping from $101K to hover around $98K.

In the bond and currency markets, a slight uptick in New York Fed inflation expectations pushed U.S. Treasury yields and the dollar higher, as traders stayed cautious about the Fed’s December rate path despite chatter about a possible 25bps cut.

FX Market Behavior: U.S. Dollar vs. Majors:

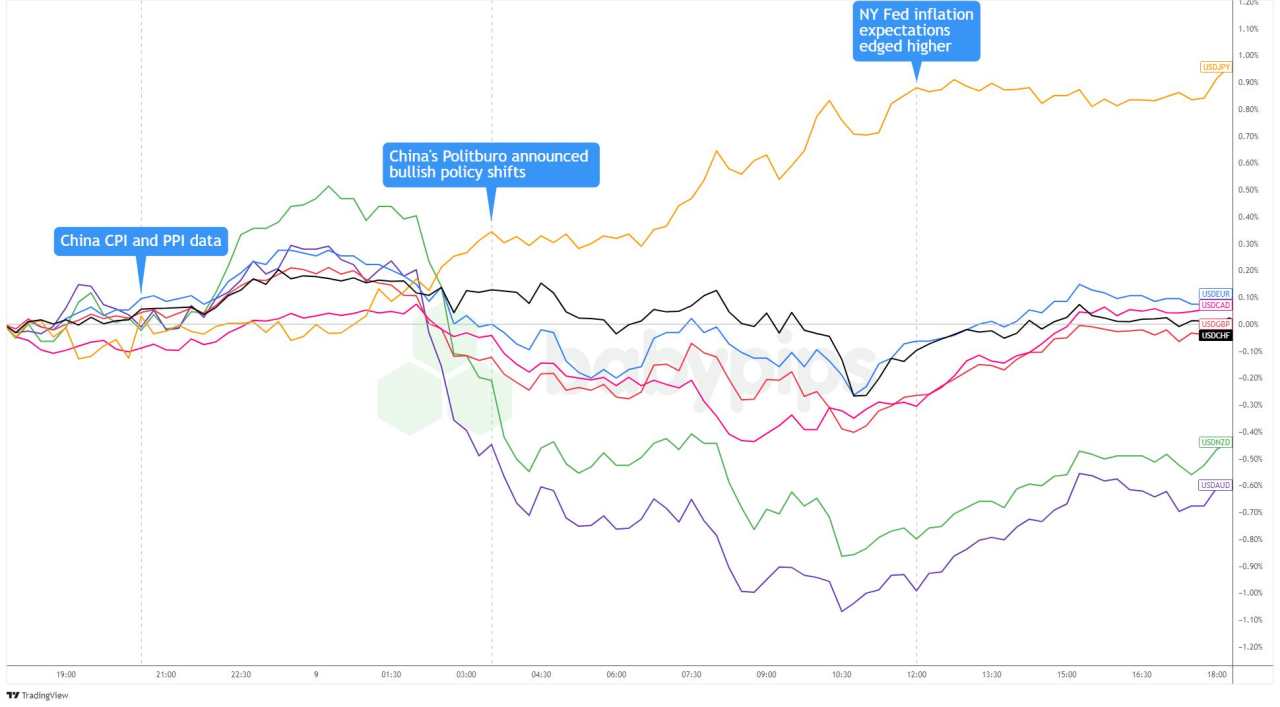

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar started the week on solid ground, bolstered by uncertainty around Syria’s leadership and weak CPI and PPI data from China, which drove demand for safe havens like the Greenback. However, the dollar slipped during early European trading after China’s Politburo signaled a fiscal and monetary push with supportive language not seen since 2011.

Dollar weakness persisted until the U.S. session, when a New York Fed report showed rising one-year and three-year inflation expectations. This spurred an uptick in 10-year Treasury yields and reignited uncertainty over the Fed’s 2025 monetary policy plans.

By the end of the day, the dollar closed mixed. USD/JPY surged to just under 151.50 after starting below 149.80, while the Greenback logged small gains against EUR, CAD, and GBP but dipped against AUD and NZD.

Upcoming Potential Catalysts on the Economic Calendar:

- Japan preliminary machine tool orders at 6:00 am GMT

- Germany final CPI at 7:00 am GMT

- Italy industrial production at 9:00 am GMT

- U.S. NFIB small business index at 11:00 am GMT

- U.S. revised nonfarm productivity and unit labor costs at 1:30 pm GMT

- New Zealand manufacturing sales at 9:45 pm GMT

- Japan BSI manufacturing index at 11:50 pm GMT

- Japan PPI reports at 11:50 pm GMT

European traders could keep an eye on Germany’s final CPI and Italy’s industrial production, as these reports could provide insights into inflation trends and economic activity within the Euro Area.

In the U.S., traders will focus on the NFIB Small Business Index and revised labor productivity and costs data, as these can shed light on economic resilience and inflationary pressures ahead of the Fed’s decision next week.

Aside from that, watch the newswires for shifts in risk sentiment ahead of this week’s awaited central bank decisions and top-tier data releases.

Make sure you’re glued to the tube in case we see increased volatility during their events, and don’t forget to check out our Currency Correlation tool when taking any trades!

Hot

No comment on record. Start new comment.